An Inverted Yield Curve

Another indicator that normally signals economic trouble ahead caught our attention this last week when the U.S. yield curve inverted. This matters because the U.S. yield curve has inverted before each recession since 1955, offering only one false signal.

Not to sound overly technical, but a yield curve in plain language is a line that plots the interest rates of bonds maturing at various times in the future. When longer-term rates drop below short-term rates, the curve is said to be inverted.

Many subtract the difference between one bond maturity and another. The question many are presently asking is, what two points on the yield curve are most relevant to compare?

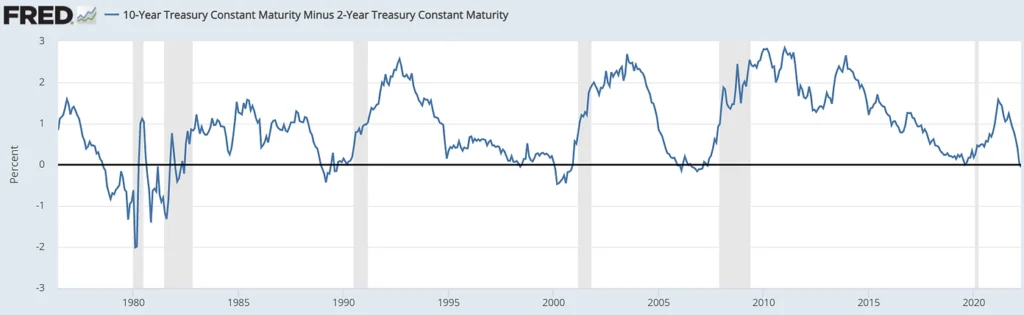

Investors historically look at the difference between the 10-year and 2-year Treasury bond yields (“10-2 spread”). When that spread turns negative, a recession historically follows within 6-24 months. As you can see below in the chart illustrating the 10-2 spread, the grey bars indicate a recession (six in total since 1980).

U.S. Federal Reserve Chair Jay Powell recently commented on the yield curve. Likely relying on a June 2018 research paper published by Fed economists Eric Engstrom and Steven Sharpe, Powell said:

Frankly, there’s good research by staff in the Federal Reserve system that really says to look at the short — the first 18 months — of the yield curve … That’s really what has 100% of the explanatory power of the yield curve. It makes sense. Because if it’s inverted, that means the Fed’s going to cut, which means the economy is weak.

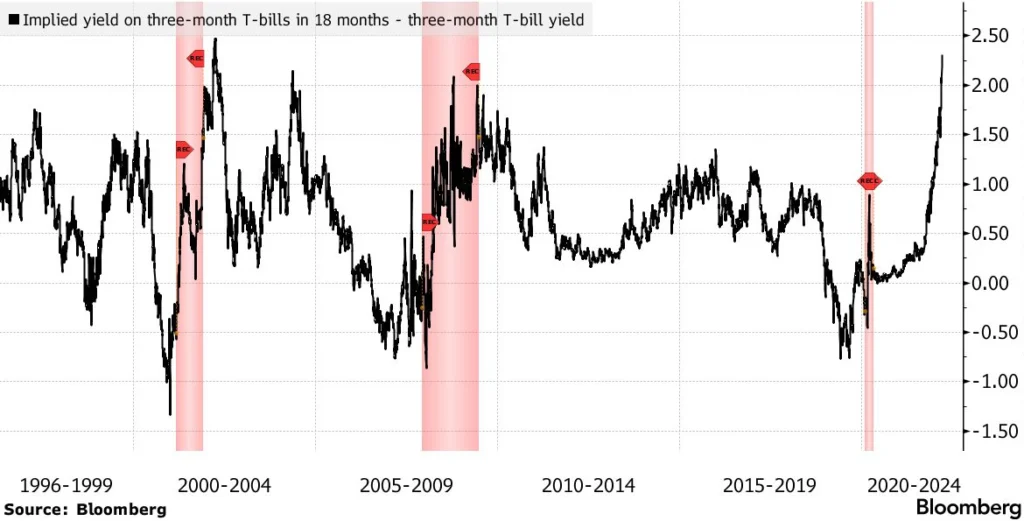

Looking at the yield curve between the implied 18-month forward rate and 3-month T-bills, the upward-sloping curve illustrates a different story than the inverted 10-2 spread.

If Powell is placing greater weight on the difference between 18- and 3-month rates, it is safe to assume to he will continue hiking rates. This is likely to further invert the 10-2 curve.

Though rate hikes can be used as a weapon to fight inflation, it can also slow economic growth. When the cost of borrowing increases on everything from mortgages to car loans, consumers have less disposable income to spend elsewhere. Furthermore, bank margins become squeezed when longer-term rates exceed short-term rates, which may deter lending.

We’ve always favoured the 10-2 spread and suggest the sentence “this time is different” are often dangerous words to follow. However, recessions do not follow an inverted yield curve immediately — it historically takes 6-24 months before a recession to happen. However, we’re avoiding growth stocks and are instead concentrating our client portfolios in conservative, dividend-paying stocks.

-written by Jeff Pollock

DISCLAIMER: The opinions expressed in this publication are for general informational purposes only and are not intended to represent specific advice. All publications have been written by a person other than the person that approved its distribution. The views reflected in this publication are subject to change at any time without notice. Every effort has been made to ensure that the material in this publication is accurate at the time of its posting. However, Schneider & Pollock Wealth Management Inc. will not be held liable under any circumstances to you or any other person for loss or damages caused by reliance of information contained in this publication. You should not use this publication to make any financial decisions and should seek professional advice from someone who is legally authorized to provide investment advice after making an informed suitability assessment.