Santa Claus is Coming to Town

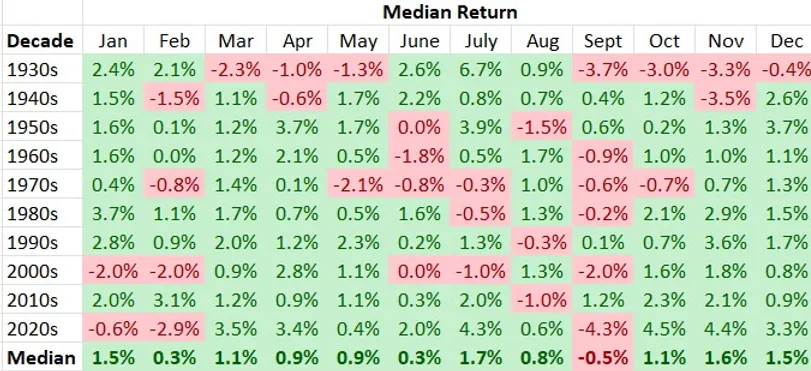

December is historically a great month for stocks.

In fact, over the last hundred years, the only decade to post a negative median return during December was in the 1930s. All decades since — from the 1940s until the 2020s — have posted a positive median price return during December.

There are several reasons that make December a strong month.

For starters, many mutual funds have an October 31 fiscal year end, which means their tax loss selling is complete by the time Halloween rolls around (November is historically a strong month for stocks too, actually).

That brings us to the Santa Claus rally, which is characterized by a strong period for stocks in the last five days of December and the first two days of January. Retail investors finish their tax loss selling in December, though many don’t wait that late to sell their losing positions.

Other factors that account for a strong December could be the optimism and/or year-end bonus that the holidays accompany.

Or, it could simply be a self-fulfilling prophecy. Every professional investor knows about the seasonal strength in December. That being the case, many will surely buy stocks over the next several weeks anticipating a December rally to unfold. If enough people follow that logic, you can be sure the market will catch a bid.

We temper our faith in seasonal trends because it doesn’t always work. After all, October is normally a strong month too, but that sure wasn’t the case this year (the S&P 500 dropped 2.2% in price).

Our Christmas list has one item. We want to see the bond market continue to price in rate cuts during the first half of 2024. As of this writing, the U.S. is expected to reduce rates on May 1 while Canada is likely to cut in March.

As rates go down, we believe equity prices – in particular, dividend-paying equity prices – will catch a bid and appreciate handsomely in value.

-written by Jeff Pollock

DISCLAIMER: The opinions expressed in this publication are for general informational purposes only and are not intended to represent specific advice. All publications have been written by a person other than the person that approved its distribution. The views reflected in this publication are subject to change at any time without notice. Every effort has been made to ensure that the material in this publication is accurate at the time of its posting. However, Schneider & Pollock Wealth Management Inc. will not be held liable under any circumstances to you or any other person for loss or damages caused by reliance of information contained in this publication. You should not use this publication to make any financial decisions and should seek professional advice from someone who is legally authorized to provide investment advice after making an informed suitability assessment.