Why Mutual Funds Often Benefit Banks More Than You

Mutual funds are marketed as safe and simple. But in reality, they often accompany hidden costs and conflicts of interest.

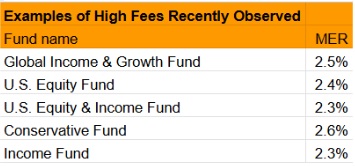

We recently reviewed a portfolio managed by another institution. The Management Expense Ratio (“MER”), which is the total cost of owning a mutual fund and is embedded in its price, was much higher than its holder anticipated.

These significant fees eat into returns annually and aren’t even tax deductible.

But high fees aren’t the only concern.

Recent findings from Canadian regulators – detailed in “Sales Culture Concerns at Five of Canada’s Bank-Affiliated Dealers” – have raised concerns about how mutual funds are sold.

The joint review by the Ontario Securities Commission (OSC) and the Canadian Investment Regulatory Organization (CIRO) found that advisors at Canada’s biggest banks often face intense pressure to meet sales targets. Unfortunately, this can lead to unsuitable product recommendations that don’t align with their clients’ financial goals.

Even more concerning:

- 24% of mutual fund sellers admitted that clients have been recommended products that aren’t in their best interest.

- 33% said clients have been given incorrect information about the products or services being recommended.

- 40% admitted that pressure from their employer directly affects the recommendations they make to clients.

As OSC CEO Grant Vingoe aptly put it: “The focus of bank representatives should be the best interests of their customers and clients – not feeling heightened pressures to meet sales targets.”

On top of that, there are gaps in advisor knowledge. The OSC and CIRO found that 23% of mutual fund advisors couldn’t even define what a MER is. While most understood that MERs reduce returns, not knowing what they are is rather alarming— especially when clients are relying on that expertise.

What We Do Differently

Putting the best interests of each client first is ingrained in our culture and legally required by the regulations governing our practice.

Because we’re 100% independent, we’re never swayed by the sales targets or product pushes that often influence advisors at large banks.

Instead of mutual funds, we build portfolios using individual securities and charge a tax-deductible management fee that is significantly lower than many mutual funds.

Each month, we send out a detailed transaction summary outlining all buys, sells, dividends, interest income, and fees for the reporting period. This means you always know exactly what you own and have greater clarity, control, and flexibility over your investments.

If you currently own mutual funds and would like a second opinion, reach out for a no-obligation portfolio review. We’ll help you understand what you’re really paying — and explore ways to keep more of your returns.

-written by Jeff Pollock

DISCLAIMER: The opinions expressed in this publication are for general informational purposes only and are not intended to represent specific advice. All publications have been written by a person other than the person that approved its distribution. The views reflected in this publication are subject to change at any time without notice. Every effort has been made to ensure that the material in this publication is accurate at the time of its posting. However, Schneider & Pollock Wealth Management Inc. will not be held liable under any circumstances to you or any other person for loss or damages caused by reliance of information contained in this publication. You should not use this publication to make any financial decisions and should seek professional advice from someone who is legally authorized to provide investment advice after making an informed suitability assessment.