Pizza Pizza Delivered a Double-Digit Return After Our Tip

As global fast food chains struggle, Pizza Pizza is quietly gaining ground—thanks in part to the growing “Buy Canada” sentiment.

Back in February 2024, we published a blog titled “We Expect Pizza Pizza to Deliver”. Given the rising food inflation, higher interest rates, and shrinking household budgets, our thesis was that cheaper food would be sought after in the coming months.

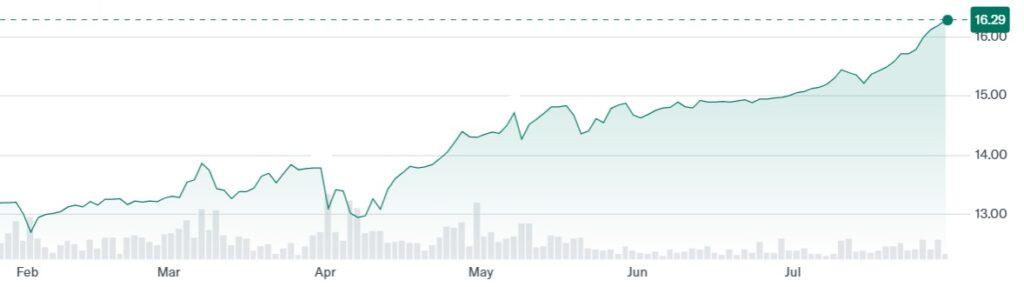

Fast forward to today, and that thesis has played out across North America. Since our blog last year, Pizza Pizza’s stock has returned 22% including dividends—and it’s up 29% so far in 2025 alone. (Disclosure: Jeff Pollock and Sunni Schneider directly and indirectly hold a financial interest in Pizza Pizza as shareholders.)

Yes, the market is up. But many fast-food restaurants have lagged Pizza Pizza. So far this year, Chipotle is down 27%; Restaurant Brands International, which owns Tim Hortons, Burger King, and Popeyes, has gained only 1.5%; and McDonalds has returned less than 4%.

Chipotle’s second-quarter earnings, reported just last week, reinforced our thesis that consumers have sought lower prices. Management acknowledged a clear customer shift toward more affordable menu items like chicken, with fewer people opting for higher-priced proteins like steak.

Despite its strong performance, we still like the stock today because consumers continue to spend conservatively.

With a dividend yield of roughly 5.8%, backed by a target payout ratio of 100% after tax, Pizza Pizza provides reliable income and moderate growth potential. In a May 2024 interview, the CEO reaffirmed plans to continue increasing the dividend. Meanwhile, management has noted rising walk-in and pickup orders as customers try to avoid delivery fees—another signal that Canadians are prioritizing value and convenience.

Although we didn’t predict a wave of “Buy Canada” sentiment, it’s now a strong tailwind. In February 2025, Pizza Pizza launched its “Reverse Tariff” campaign, offering a 25% discount on regularly priced pizzas using the code REVERSETARIFF. Sales surged more than 20% in just one weekend, and the campaign earned national media attention and viral social traction. With nearly all ingredients sourced domestically (except California tomato sauce), Pizza Pizza’s local focus is resonating.

Structurally, the royalty model remains compelling. The parent earns 6% of sales from Pizza Pizza restaurants and 9% from Pizza 73, while franchisees take on all the operating risk by covering day-to-day expenses.

For investors that want a royalty in their portfolio, the options are becoming scarce. Fairfax Financial acquired The Keg while A&W restructured last year, eliminating two royalty investment stocks.

That said, the stock isn’t without drawbacks—its dividend was cut in 2020 during the pandemic, and there’s limited analyst coverage. But for investors focused on value, income, and consistency, Pizza Pizza continues to deliver—both at the register and in the portfolio.

-written by Jeff Pollock

DISCLAIMER: The opinions expressed in this publication are for general informational purposes only and are not intended to represent specific advice. All publications have been written by a person other than the person that approved its distribution. The views reflected in this publication are subject to change at any time without notice. Every effort has been made to ensure that the material in this publication is accurate at the time of its posting. However, Schneider & Pollock Wealth Management Inc. will not be held liable under any circumstances to you or any other person for loss or damages caused by reliance of information contained in this publication. You should not use this publication to make any financial decisions and should seek professional advice from someone who is legally authorized to provide investment advice after making an informed suitability assessment.