Aecon Group Will Help Power Canada’s Next Infrastructure Boom

Canada is entering a historic infrastructure boom. Electricity demand is expected to surge 25% by 2030, driven by artificial intelligence, electrification, and manufacturing. Aecon Group is perfectly positioned to build the critical infrastructure required to meet this exploding need. (Disclosure: Jeff Pollock and Sunni Schneider directly and indirectly hold a financial interest in Aecon Group as shareholders.)

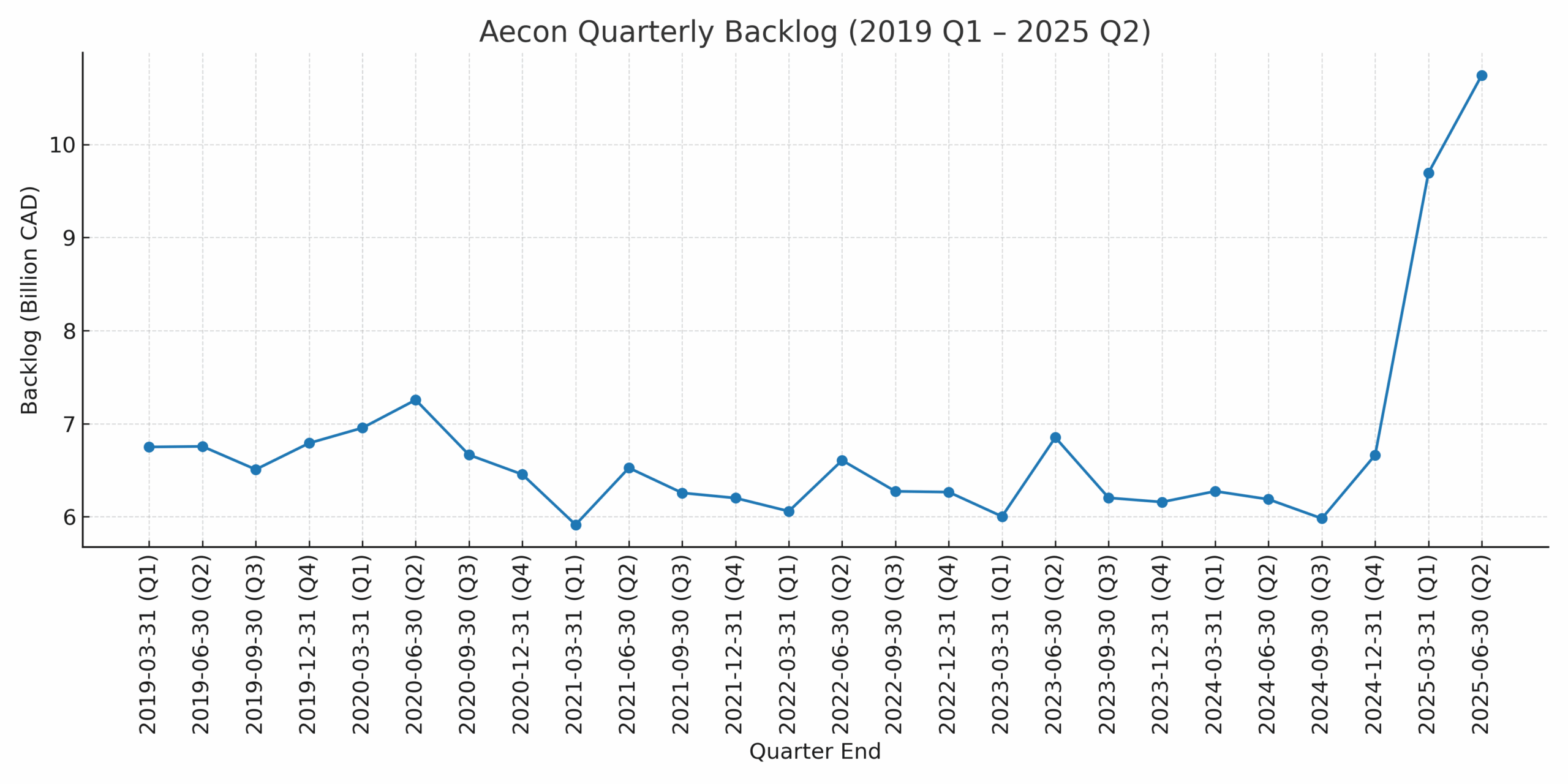

CEO Jean-Louis Servranckx recently said he’s “not worried about [revenue]”—and with good reason. Aecon’s backlog—the work they’ve been hired to do but haven’t finished yet—has soared to a record $10.7 billion. For context, the company generated $4.2 billion in revenue last year.

The backlog includes power infrastructure projects. For example, Aecon is a key partner in constructing new reactors at Ontario’s Darlington Nuclear Generating Station. This will help support energy-intensive uses like the data centers that power artificial intelligence.

We initially purchased the stock at $10.55 per share in July 2023. Factoring in the dividend, which yielded 7.2% at that time, clients have enjoyed a total return of approximately 110%. Back then, the market was distracted by cost overruns, and the stock fell more than 20% in the three months leading up to our purchase.

The Coastal Gaslink in B.C., the Gordie Howe Bridge in Windsor, and the Eglinton and Finch LRTs in Toronto were all “fixed price” contracts (meaning the company received a set amount regardless of actual costs), and expenses had spiraled beyond expectations.

Nevertheless, we knew these projects would eventually finish and the selloff was a buying opportunity.

Those challenges are now largely behind them. The Coastal Gaslink is complete, and the remaining projects are on track for year-end completion (yes, even the Eglinton LRT).

Critics argue that construction is low margin. However, Aecon has shifted its contract mix aggressively to favour “cost-plus” agreements (meaning the company gets paid for all its costs plus an agreed profit), which now represents 76% of the backlog—up from 50% a year ago. This pivot will reduce the risk of profit margins getting clobbered by cost overruns.

Aecon’s dividend has grown—from $0.05/quarter in 2011 to $0.19/quarter today—and was never cut during the pandemic, even when many other companies reduced or eliminated their payouts.

Recent insider buying by company brass further underscores confidence in Aecon’s future. In fact, one director just bought $118,000 worth of stock earlier this month.

With the risk from old legacy projects fading, a safer contract mix in place, and surging demand for power infrastructure, Aecon remains a core growth-and-income holding. We’re maintaining our position and are adding this stock for new client portfolios.

-written by Jeff Pollock

DISCLAIMER: The opinions expressed in this publication are for general informational purposes only and are not intended to represent specific advice. All publications have been written by a person other than the person that approved its distribution. The views reflected in this publication are subject to change at any time without notice. Every effort has been made to ensure that the material in this publication is accurate at the time of its posting. However, Schneider & Pollock Wealth Management Inc. will not be held liable under any circumstances to you or any other person for loss or damages caused by reliance of information contained in this publication. You should not use this publication to make any financial decisions and should seek professional advice from someone who is legally authorized to provide investment advice after making an informed suitability assessment.